Comparing indexed options between industry super funds

Although fees are an important factor to consider when choosing a super fund, there are other considerations that people should be aware of. On top of fees, I’ll also be comparing index & market exposures and ESG implementation. I’ll also be explaining how Rest achieves 0% fees for their indexed options.

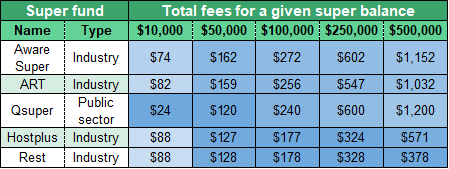

Fees

Below are tables taken from my spreadsheet (as at January 2024, please refer to the spreadsheet for up-to-date figures):

Index & market exposures

Although the super funds generally invest in the same companies, there are some subtle differences because of the indexes they follow. The indexes the super funds follow are listed below:

| Name | Australian shares | International shares |

|---|---|---|

| Aware Super | Aware Super Custom Index on MSCI Australia Shares 300 | Aware Super Custom Index on MSCI World ex-Australia |

| ART | S&P/ASX 300 Total Return Index | MSCI ACWI ex-Australia with Special Tax Net Index in $A |

| Qsuper | S&P/ASX 200 Accumulation Index | MSCI World ex-Australia Index, hedged |

| Hostplus | S&P/ASX 200 Accumulation Index | MSCI World ex-Australia Index |

| Rest | S&P/ASX 300 Accumulation Index | MSCI World ex-Australia ex-Tobacco Index |

Notes:

- Aware Super’s indexes are custom as they changed the index for sustainability and ESG considerations.

- “Special Tax” in ART’s international shares option means that the index takes into account the favourable tax environment that exists in super funds.

Below is a table of how much of the market someone can capture when using the DIY options in each super fund, where green are markets that are covered by Australian shares and International shares and red are markets that are not covered:

Notes:

- I further elaborate on the use case of International hedged shares in this article: Should Australians use hedged international equites?

ESG

ESG investing aims to overweight companies that have favourable Environmental, Social, and Governance characteristics and underweight companies that show unfavourable characteristics. However, the drawback to ESG is the expected lower return and risk, as detailed in this article. This type of investing deviates from a pure passive portfolio, but can suit those who prefer to overweight towards “greener” companies. Although, there is evidence by Hartzmark and Shue (2023) that ESG investing may be counterproductive to making “brown” firms more green.

The table below shows how the super funds handle ESG:

| Name | ESG |

|---|---|

| Aware Super | Restrictions/exclusions to tobacco, thermal coal, and controversial weapons. Also excludes or has a reduced weighting to carbon intensive companies. More information can be found in their Investment and Fees Handbook. |

| ART | Exclude companies that manufacture tobacco and companies with any involvement with cluster munitions and landmines. They also aim to reduce their carbon exposure. More information can be found here. |

| Qsuper | Almost identical ESG implementation to ART super. |

| Hostplus | Excludes investment in controversial weapons. This can be found in their Member Guide, found under the Responsible Investing section. |

| Rest | No ESG integration with no other negative screenings apart from tobacco. |

Rest’s 0% fee indexed options

Most indexed options follow their respective index by investing directly in the companies described by the index. Rest Super is the exception to the other super funds mentioned, where they use the following funds: Macquarie True Index Australia Shares and Macquarie True Index International Equities Fund. The funds use derivatives (specifically total return swaps) to follow the index, introducing counterparty risk if Macquarie Bank defaults on their derivative contracts. The funds also hold an underlying fund, retaining any outperformance and compensating for any underperformance. The underlying fund for Macquarie True Index Australian is Macquarie Equity Index Fund. For Macquarie True Index International the underlying is Macquarie International Equities Fund (found on page 24 of this annual report with credit to u/redditau34 for finding this).

The uncertainty of how much counterparty risk there is and how comfortable one is with the risk should be considered when using Rest’s indexed options, even if Rest is comfortable with the risk that comes with using derivatives. The funds by Macquarie do have about $2 billion in assets (as at 31/12/2023), and so these funds are unlikely to close. Below is a screenshot of how the derivative contracts work, taken from Macquarie True Index International Equities Fund’s PDS:

Apart from the counterparty risk, there are other consequences of using derivatives to track the index that are not immediately obvious.

The biggest one is to do with the International True Index fund. The objective of these True Index funds is to have the pre-tax return of the fund equal the return of the index they’re tracking. On the surface this seems perfectly fine, as this is just the objective for all index funds before fees, including index funds that physically buy the companies. However, for some unknown reason, index providers assume the worst possible tax scenario for their international indices that does not reflect reality.

For example, index providers will assume that US dividends get taxed at 30% when, in reality, they only get taxed at 15% because of Australia’s tax treaty with the US. You can clearly see this happening when you look at the performance of VGS or BGBL, where they effortlessly outperform their benchmarks despite them just being passively managed ETFs. So, what this means for Macquarie’s International True Index fund is that in trying to match the return of the index, it also inherits these worst possible assumptions.

To get an idea of how much the difference is between the index returns and actual fund returns, below are the returns of VGS ending March 2026 (managed fund version with inception date 06/06/1997):

Taking the difference between its gross returns (before MER and transaction costs) and the index returns, the index appears to overestimate costs by around 0.20% to 0.35%. I did not find any evidence that there is a hidden cost for the Macquarie’s Australian True Index fund, so if you’re allocating 30% to Australia, the actual total cost would be around 0.14% to 0.245% and not 0%.

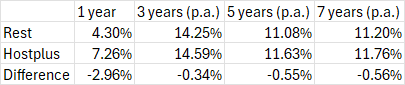

This seems to be supported by comparing the returns between Hostplus International Indexed option and Rest’s International Indexed option ending March 2026:

Usually performance of indexed options between super funds doesn’t match exactly because of different indexes or minor differences in company composition. Ignoring the 1-year performance, the consistent gap in performance could be explained by the 0.20% to 0.35% hidden cost. The performance gap could also be explained by the Macquarie True Index funds distributing more income and so paying more tax. In either case, this suggests Rest would be one of the most expensive super funds for indexed options, at least within industry super funds.

For the Australian True Index fund, there is a bit of weirdness as u/VGSsilverfox claims that it does not pay franking credits, but Rest “subsidises” this from Rest’s other investments. I don’t see if this statement can be proven, as we would either need to get the tax components from the distributions of the fund or be able to see what companies are being held in the underlying investments.