Super investing – A quick guide

The majority of people are disengaged with how their retirement savings are invested. But even spending a bit of time educating yourself and making sure you’re on top of your super could potentially save you over $100K, even more so the younger you are. Engaging with your super doesn’t even take much time. Realistically, you’ll only need to spend at most a couple hours setting up your super initially, and then you can set and forget until you start getting close to accessing your super in your 60s.

In less than 10 minutes, I’ll explain three main things to consider when deciding to invest your super:

- Management Style

- Fees

- Asset Allocation

Management Style

For every super fund, they will have different investment options, each option will have different types and amounts of assets they invest in. There are two main management styles an investment option can have:

- Active management involves actively buying and selling assets in an attempt to beat a market benchmark.

- Passive management matches the performance of a market benchmark, involving very minimal buying and selling.

You will see that actively managed options tend to say something to the effect of ‘beating the market benchmark’ in the investment description or objective, whereas passively managed options will say something like ‘matching the market benchmark’. Investment options may also have the word ‘indexed’ in their name to signal they are passively managed.

Because active management employs fund managers and researchers to try to beat the market, it incurs significantly higher fees than passive management. But are these higher fees worth it?

Both theoretical and empirical evidence overwhelmingly suggests that passive management beats active management over the long term. I go into more detail in my article: Why index funds are the optimal place to start. Australian academic research on super funds similarly favours passive over active, finding that the higher costs generally lead to lower returns (Drew and Stanford, 2002; Sy, 2008; Basu and Andrews, 2014; Niblock et al., 2017).

To further illustrate the long-term underperformance of active management, the SPIVA Scorecard shows that 84% of active funds underperformed the Australian market over 15 years (data as of 31 Dec 2022).

Fees

You may often hear that it is best to go for low fees when choosing a super fund, as also mentioned by Moneysmart. But how much of a difference do fees really make?

First, let’s go through the different types of fees you’ll find in a super fund. The most common types of fees and costs are:

- Admin fees – the cost of maintaining the infrastructure of the super fund. The fee can be a fixed $ amount and/or a percentage of your investments.

- Investment fees and transaction costs – the cost of managing an investment option automatically subtracted from the investment’s performance.

- Insurance fees – the cost of having different types of insurance cover in your super. Learn more about insurance from Moneysmart.

In the Super sting: how to stop Australians paying too much for superannuation report by Minifie, Cameron, and Savage (2014), they show that:

- An extra 1% fee can reduce retirement income by more than 20%.

- High fees often did not result in better performance, nor did it reduce investment risk.

- The best guide to future performance is low fees, not strong past performance.

Mahaney (2023) similarly finds that on average, a 1% fee during retirement results in a 15% reduction in retiree income and a 23% reduction in inheritance amount. So in general, you are more likely to be better off by focusing on low fees.

But with so many super funds and investment options, trying to compare fees across all these options would be extremely time-consuming. That’s why I manage a Super Fund Comparison Spreadsheet that compares fees (excluding insurance fees) across the most popular super funds for Australian shares, International shares, and High Growth options. I try to update the spreadsheet once or twice a year, but fees don’t usually change too often. Note that I do have a Performance tab; however, this is purely for data-collecting purposes, and as mentioned before, low fees are a better indicator of future performance than strong past performance.

Asset Allocation

Super funds will generally offer you three types of options:

- Diversified/premixed options will invest in a variety of assets chosen and managed by the fund managers, and so the option suits people who aren’t very knowledgeable about investments. Super funds will generally have the following premixed investment options, sorted from least risky to most risky:

- Conservative – typically 30% – 50% growth assets and 50% – 70% defensive assets.

- Balanced – typically 50% – 75% growth assets and 25% – 50% defensive assets.

- Growth – typically 75% – 100% growth assets and 0% – 25% defensive assets.

- DIY options are for people who want more flexibility with how their investments are allocated. Some common DIY options include:

- Equities – Australian shares and International shares. Considered a growth asset.

- Bonds – Australian and International bonds and other fixed income assets. Considered a defensive asset.

- Cash – short-term money market securities and some short-term bonds. Considered a defensive asset.

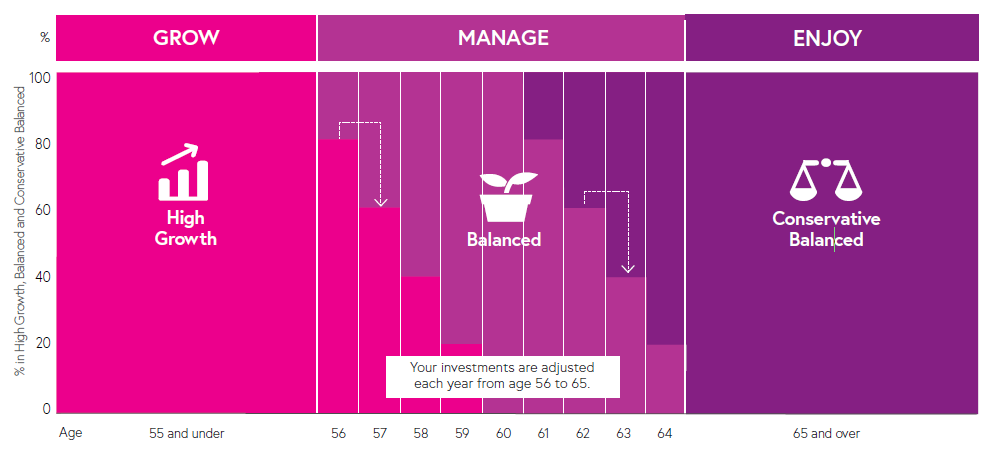

- A Lifecycle option is generally set to a High Growth premixed option when you’re young and gradually transitions to a lower-risk portfolio as you approach retirement. This investment option is ideal for people who want a hands-off approach to super and do not have to tinker with allocations when approaching retirement. Below is an illustration of Aware’s Lifecycle option.

So which investment options should you choose? This is a difficult question to answer, as everyone will have different preferences relating to their circumstance and age, as well as different perceptions and tolerance to risk. Although academic research over the past 30 years has made great strides in understanding what investments people should have, even today there are still debates on what is the best way to invest.

Below are my general guidelines:

- Equities are generally recommended to be held over long periods, and over long periods they generally perform better than bonds and cash (refer to this article I wrote for more details). Because of this, it makes sense for those younger than 40 to be in 100% equities. If doing a DIY approach using Australian shares and International shares, to decide on how much to allocate to each, refer to my article: What Australian/International allocations should you choose?

- In the short term, bonds and cash are considered less risky than equities, and so it makes sense to allocate a portion to these safer investments when withdrawing your super. However, allocating too much to these safer investments can actually leave you worse off because your portfolio doesn’t have enough growth to sustain withdrawals. The most well-known retirement allocation in finance is the 60/40, 60% equities and 40% bonds, and it is a good place to start.

- To transition from a 100% equities portfolio to your desired retirement portfolio, it can make sense to slowly introduce safer investments when you’re getting close to accessing your super. Lifecycle options do this automatically, where they tend to start transitioning to their retirement portfolio 10 years before you draw on your super. However, the problem with Lifecycle options is that most of them are actively managed and so can be quite expensive. If you’re willing to put in the work though, it isn’t too hard to do this yourself.

- A common mistake I see people make is switching all their investments to cash when the market is falling or during times of uncertainty in hopes of protecting their portfolio. DO NOT EVER DO THIS. This is what we call in finance “timing the market,” and research has shown this strategy tends to underperform someone who simply does nothing (Felix and Warwick, 2021; Cao, Chong, and Villalon, 2025). In the words of Peter Lynch: “Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.”

Summary

- Use passively managed investment options.

- Prioritise cheap fees (refer to my spreadsheet).

- Decide what assets to invest in, how your allocations change over time, and stick to the plan!

If you want cheap, passively managed options, refer to my next article: Comparing indexed options between industry super funds.

June 2026 note: Rewrote this article I wrote three years ago. PIA wrote a similar article that helped me with structuring this article; if you want to check it out: How to invest your super – Passive Investing Australia.