DFA and Avantis: The father and son of factor investing

In the previous article, A Koala’s Guide to Factor Investing, I went through what factor investing is, the theory, the possible explanations for their existence, and some considerations if one wants to allocate to risk-premia factors. But how should one go about allocating to risk-premia factors?

If you view discussions on factor funds in the Rational Reminder Community, the two names you’ll see appear the most are Dimensional Fund Advisors or DFA (co-founded by David Booth) and Avantis (co-founded by Eduardo Repetto). But why are these two fund managers the most popular for factor funds? Let me first take you through the history of how DFA and Avantis were founded.

History

The 1960s was the birth of modern finance that brought forth revolutionary ideas and concepts. Jensen (1967) was one of the first, if not the first, to find that a significant majority of active fund managers underperform the market, suggesting that passively holding the market would be a more successful strategy.

This led Mac McQuown and his team at Wells Fargo to create the world’s first index fund in 1973. However, the funds were only available to institutional investors due to regulations. One of the people who helped McQuown with creating the index fund was David Booth, who at the time was friends with John Bogle (RRP, #43). Booth played a role in convincing Wells Fargo to pass on their learnings to John Bogle, leading Bogle to create Vanguard and launch the first index fund available for retail investors in 1976.

Later on, as Booth learned more about the business, he knew how great index funds are conceptually but thought they were too rigid and could see the value in a more flexible implementation (RRP, #131). He also noticed a gap in the market where all the institutions were holding large-cap US stocks when they could benefit from holding small caps to be more diversified. This led to him founding Dimensional Fund Advisors (DFA) in 1981, alongside Rex Sinquefield, and launching the first small-cap index fund.

IIt was around this time when research started to find anomalous returns in certain types of stocks, leading DFA to quickly implement this new research into their funds. DFA was so on top of incorporating the latest research that when Fama gave Booth the draft of his paper he’d been working on with Ken French, where they added Value and Size to create the Fama-French 3 Factor model, DFA was able to release Value funds before the paper was officially published (RRP, #131). DFA also worked and consulted with academics who later on became Nobel laureates (DFA, 2026):

- Eugene Fama: known as the “father of modern finance” for formalising the efficient market hypothesis and, alongside Ken French (who DFA also consults with), created the Fama-French asset pricing models.

- Merton Miller: laid the foundation for corporate finance theory with his Modigliani–Miller theorem and wrote the paper demonstrating the irrelevance of dividends.

- Myron Scholes and Robert Merton: formulated the Black–Scholes Formula to determine the value of derivatives.

- Douglas Diamond: considered a founder of modern banking theory and is most known for his research on financial crises.

This is what sets DFA apart from other fund managers. Keeping up, contributing, and incorporating financial science into their products while having connections to some of the most influential figures in finance.

In 2017, co-CEO and co-chief investment officer Eduardo Repetto at DFA left the company so that he could spend more time with his family. It was during this time when American Century offered Repetto to work with them to create a direct competitor to DFA. This proposition appealed to Repetto, as he liked the challenge of starting on a clean slate, and his wife liked how American Century pays some of their profits to a non-profit research organisation because of their ownership (Southall, 2019).

Repetto, alongside Patrick Keating, who also worked at DFA, launched Avantis Investors. Repetto then poached another five DFA employees to help with the operations of Avantis (Southall, 2019). Now, as of December 2025, Avantis has reached $100 billion AUM from their global operations. For reference, DFA has around $800 billion AUM and Vanguard is around $11 trillion AUM.

Avantis may not have the history and connections that DFA does, but they do share the same core values and are both best known for offering actively managed factor funds. But why are DFA and Avantis so highly regarded when most active managers underperform the market over the long term?

Why do active managers underperform?

It is very well known that most active managers underperform the market over the long term. In fact, SPIVA reports around 80% to 90% of active managers underperformed the market over the last 15 years ending FY 2025. A reasonable takeaway is to avoid active funds, given how unlikely it is to pick a winner if you picked randomly. This is also a very good reason why most people should use passively managed funds. However, there is a bit more to the underlying reason for the majority of active managers to underperform.

Bessembinder et al. (2022) found that the average return of an active manager does outperform the market over the long term, but only before fees. It is only after considering the high fees that the majority of active funds underperform. This implies that active managers who are able to control their fees stand a better chance of outperforming. This seems to be supported by Huang et al. (2022), who found that for the very few funds that outperformed the market in their sample, some of the common characteristics among the funds are lower expense ratios and lower turnover.

Active and passive management is also not black and white. It is more like a spectrum where DFA and Avantis, despite being labelled as active managers, arguably possess more passive qualities. Larry Swedroe argues this point in his article, The False Dichotomy: Why the Active vs. Passive Fund Debate Misses the Point.

What makes DFA and Avantis stand out?

Efficient factor targeting

DFA and Avantis stay very true to the academic literature by using metrics that are robust, whereas factor funds that follow an index often have suboptimal implementation (Blitz, 2016).

For example, DFA and Avantis both use some form of book-to-market equity (B/M) as their only proxy to Value. The reason they don’t use a combination of Value metrics that other funds may do, like VVLU and MSCI factor indexes, is because DFA’s internal research finds B/M to be the most robust proxy for Value. Alternative Value metrics like earnings-to-price, cash flow-to-price, and sales‑to‑price also tend to have more turnover (Ben Felix links to DFA’s 2016 paper here).

Furthermore, most other active managers or factor indexes like MSCI target the Quality factor, which involves combining multiple “quality” metrics. However, Novy-Marx and Medhat from DFA (2025) find that these quality metrics are noisy proxies for Profitability and that targeting Profitability directly, like DFA and Avantis are doing, is superior.

Moreover, active management is undoubtedly the most efficient way to get factor exposure. The advantages of actively managed factor funds over factor index funds include reducing factor decay (Flint and Vermakk, 2022), minimising rebalance timing luck (Hoffstein et al., 2020), and the ability to trade tax advantageously (Chen and Israelov, 2025).

Addresses problems with index funds

Although index funds are a great innovation that outperforms the majority of active managers over the long term, there are small but material inefficiencies with how these indexes are constructed. Sammon and Shim (2025) explore the magnitude of these inefficiencies in their paper, Index Rebalancing and Stock Market Composition: Do Indexes Time the Market?

Indexes are required to quickly respond to stock market composition changes, like issuances, buybacks, and IPOs. However, companies issue stocks if they think their share price is high and buy back if their share price is low, so indexes are effectively buying high and selling low when they need to adjust these companies back to their market-cap weighting. IPOs also tend to start with high valuations, resulting in poor returns (Ben Felix has a video on IPOs here).

Quickly incorporating insurances, buybacks, and IPOs into indexes contributes to negative factor loadings on Value, Profitability, and Investment. Because of this, they found rebalancing every two years saved at least 0.50% annually. This is why DFA (and likely Avantis as well) excludes companies that issued stocks and recent IPOs (RR, #360).

DFA vs Avantis

Although they share the same DNA in their investment philosophies, there are subtle differences in how they operate and implement these ideas into their funds. Below is a summary of some of the differences that I could find:

- History: DFA has a significantly longer and proven track record, being around for over 40 years now, versus Avantis, which started almost 10 years ago.

- Research: DFA has a research department; they themselves have read the majority of factor-based research and thought of just about everything to test. On the other hand, Avantis rely more on the academia rather than hiring a big team of PhD researchers.

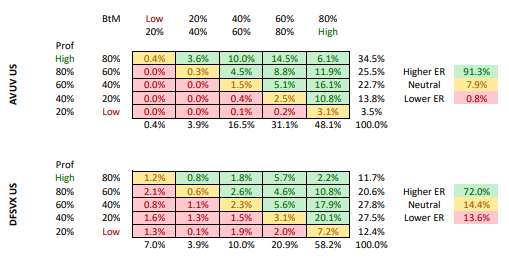

- Value funds: For funds that are labelled as ‘Value’, DFA primarily targets Value using B/M as a proxy, while Avantis uses joint adjusted B/M and profitability at a roughly equal split. Avantis published their own research conducted by Wahal and Repetto on why they believe joint value and profitability are superior, first using US data in their 2020 paper and then international data in their 2021 paper. This difference in methodology means that DFA would have a higher exposure to Value while Avantis would have a higher exposure to Profitability. To give a visual on how DFA and Avantis approach Value funds differently, Luke_Swanson made this comment in the Rational Reminder Community, sharing an email they received from Avantis analysing the company composition broken down by Value and Profitability between their Avantis US Small Cap Value ETF (AVUV) vs DFA’s US Small Cap Value Fund (DFSVX).

- Profitability: DFA uses operating profitability, while Avantis uses cash-based profitability that removes accruals. There has been some contention on which metric best captures profitability. Avantis cites Ball et al. (2015), who found that cash-based profitability performed slightly better than operating profitability. However, DFA’s internal analysis finds this result is not pervasive outside the US and that operating profitability is a better proxy for profitability. Since accruals relate to investment, DFA finds cash profitability performs no differently than operating profitability while controlling for investment (Ben Felix links to the 2020 DFA paper here).

- Sector tilts: Avantis chooses to tilt across sectors and apply a 30% sector cap, instead of tilting within sectors (sector neutrality). DFA has some limit that a sector can deviate from its market weighting.

- Transparency and attitude: Avantis has published their general methodology in their Our Scientific Approach to Investing and are generally more open to posting resources. This is a stark contrast to DFA, who are more tight-lipped, and the public only hears snippets of their methodology through interviews. Avantis, although their primary business is working with financial advisors, are willing to cater towards retail investors. This has been evident when Avantis launched their company and was able to offer factor ETFs before DFA. The trend of DFA’s complacency towards retail investors continues here in Australia, where despite them operating in Australia since 1994, they only began listing their products on the ASX at the end of 2023, and these products are still managed funds rather than ETFs. Two years later and Avantis was able to beat DFA in offering ETFs to Australians. Avantis also beat DFA to the punch in Canada as well.

- Securities lending: DFA tends to do more securities lending than Avantis as calculated by Ben Felix here, at least in the US, but it is unconfirmed if the same applies to DFA in Australia.

- Fund structure in Australia: DFA lists some of their managed funds on the ASX (not true ETFs), while Avantis ASX-listed ETFs hold Ireland-domiciled accumulating ETFs. Although these accumulating ETFs are not expected to pay any distributions to investors for them to pay tax on, there is a risk that the ATO may change their stance in the future.

- Tax drag and after-tax costs: DFA funds are all directly holding the companies, so they do not suffer any tax drag. Although they are managed funds and so supposed to be less tax efficient than ETFs, Mancell Financial Group calculates the tax cost for DFA’s core funds to be less than the Vanguard equivalents. The Avantis ETFs do suffer from tax drag, as Australians are unable to recover the withholding tax. However, because there is no distributed income to pay tax on, the tax drag cost is expected to be less than an equivalent fund that doesn’t have tax drag but investors need to pay tax on distributions.

Fund Options

After considering the differences between DFA and Avantis, below is a comparison between the Aus-domiciled DFA and Avantis funds.

An alternative is to use IBKR to buy US-domiciled DFA/Avantis ETFs, as they have cheaper MERs and have tighter spreads. However, the US takes 15% tax from ex-US dividends (won’t happen with the Ireland-domiciled accumulating ETFs) and you’re paying tax on the dividends. Instead, you could directly buy the Ireland-domiciled accumulating ETFs that the Avantis ETFs hold if you don’t mind the inconvenience for a 0.08% or 0.10% cheaper MER.

Australia

| Ticker | Name | AUM | MER |

|---|---|---|---|

| DACE | Dimensional Australian Core Equity Trust – Active ETF | $6.8 billion | 0.279% |

| DAVA | Dimensional Australian Value Trust – Active ETF | $1.5 billion | 0.335% |

International Core

| Ticker | Name | AUM | MER |

|---|---|---|---|

| DGCE | Dimensional Global Core Equity Trust (Unhedged Class) – Active ETF | $9.3 billion | 0.301% |

| DFGH | Dimensional Global Core Equity Trust (AUD Hedged Class) – Active ETF | $9.3 billion | 0.301% |

| AVTG | Avantis Global Equity Active ETF | $6.72 million | 0.30% |

International Factor Tilt

| Ticker | Name | AUM | MER |

|---|---|---|---|

| DGVA | Dimensional Global Value Trust – Active ETF | $1.1 billion | 0.400% |

| DGSM | Dimensional Global Small Company Trust – Active ETF | $673.9 million | 0.552% |

| AVSV | Avantis Global Small Cap Value Active ETF | $11.49 million | 0.49% |

Emerging Markets

| Ticker | Name | AUM | MER |

|---|---|---|---|

| AVTE | Avantis Emerging Markets Equity Active ETF | $9.04 million | 0.45% |

You can view the calculated factor loadings here: Factor Regressions for Australian Funds