Should Australians use hedged international equites?

Investing in international equities for an Australian involves taking on currency risk. So, on top of your returns being affected by the performance of those assets but also any exchange rate movements with that asset’s currency with the AUD. International equity funds that take on this currency risk are referred to as unhedged, while funds that remove this currency risk are labelled as hedged.

Because of currency risk, for example, it is possible for the performance of the assets to be positive, but the AUD also appreciating against the foreign currencies caused the unhedged return to be less positive or even negative. In general, AUD appreciating against the foreign currency benefits hedged equities, while AUD depreciating against the foreign currency benefits unhedged equities. But how bad is currency risk for Australians?

Currency risk and volatility

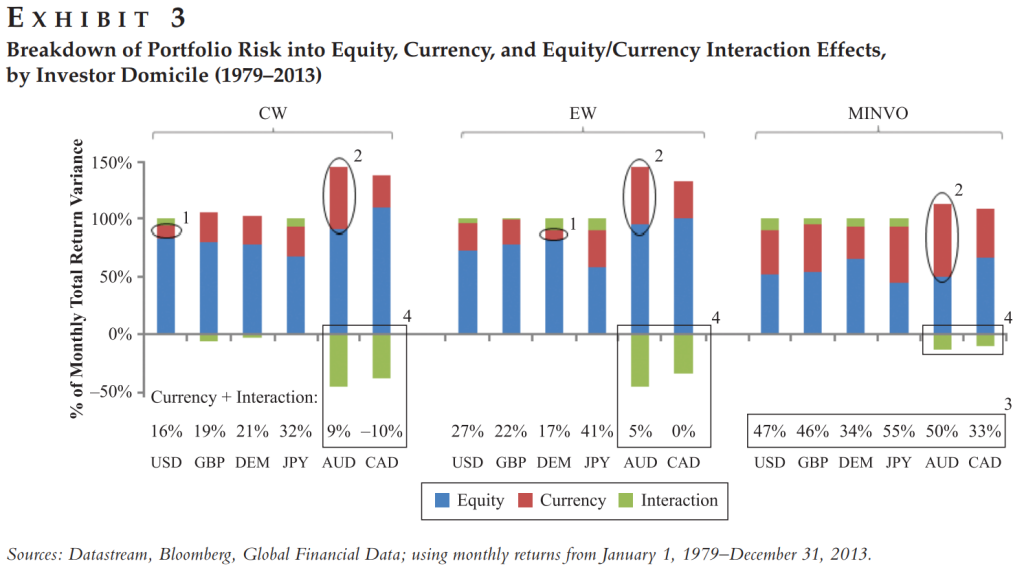

The effectiveness of hedging at reducing portfolio volatility is dependent on the nature of the currency. De Boer (2016) shows that for natural-exporting countries like Australia and Canada, their currencies appreciate at the same time as when global equity markets are doing well and vice versa. It is because of this interaction between home currency and global equity returns that naturally dampens the volatility of unhedged and makes 100% hedged more volatile.

The author shows this in the chart below, specifically the left-most chart that shows market-cap weighted portfolios. For an Australian investor, the interaction between their home currency and global equity returns helps counteract some of the equity and currency volatility.

To see this in action, the below table compares the drawdowns (from peak to bottom) and recovery durations (from bottom to original price) for unhedged and hedged MSCI World ex Australia. Across the major market drawdowns since 2000, hedged had worse drawdowns than unhedged. On the flip side, hedged typically recovered faster than unhedged, where unhedged was unable to recover after the dot-com crash before being hit again with the GFC crash. The takeaway is that the additional volatility of hedging is a double-edged sword, lower lows when AUD falls with global equities but also higher highs when AUD rises with global equities.

| Drawdown | Recovery Duration | |||

| Unhedged | Hedged | Unhedged | Hedged | |

| Dot-com (2000 – 2002) | -46% | -48% | N/A | 41 months |

| GFC (2007 – 2009) | -38% | -51% | 56 months | 47 months |

| Covid (2020) | -13% | -21% | 8 months | 5 months |

| Rising global interest rates (2021 – 2022) | -16% | -24% | 12 months | 16 months |

Although 100% hedged is more volatile than 100% unhedged, partially hedging a portfolio can help reduce the overall portfolio’s volatility. Note that hedging is not a free lunch, as hedging reduces returns from hedging costs (Vanguard had previously found this to be around 2 to 6 bps or 0.02% to 0.06%). de Roon et al., (2012) also argue that hedging reduces the weight of currencies with high expected returns, with the caveat that Australia was least affected by this in their sample, the monthly return decreasing by 0.01%.

How much hedging?

Unfortunately, there is no clear answer on how beneficial hedging can be to a portfolio, which is not helped by how sparse the topic is in the academic literature from my research. Likewise, there is no strong evidence that I could find that suggests that your portfolio should be X% in AUD when adding up your Australian equities and International hedged equities.

Some general guidelines are that currency fluctuations even out over the long term, say 20+ years, so hedging would be more beneficial for short-to-medium time horizons. Moreover, hedging could be used if the investor believes that the AUD will appreciate during the time they are hedged, typically hedging if the AUD/USD is below its historical average. However, I would caution against this, as it is borderline market timing and may lead to unnecessary complexity in your investment strategy.

To get a feel for how others approach hedging:

- In superannuation, the average proportion of hedged to unhedged International was around 20% to 30% from 2013 to 2023 (APRA, 2026). Their total AUD exposure from their equities was also around 50% to 60%.

- For VDAL, as of April 2026, VDAL’s target hedged International proportion was around 38% with its total AUD exposure to be around 58%.

My personal feeling and how I view AUD exposure in equities: in an interview with Cederburg that discusses his paper, specifically the finding that 33% to your home country is optimal, he hypothesises that this could mainly be to get exposure to your home currency. The paper also finds 10% to 55% performs very similarly to the optimal allocation, and so how I interpret this result is that it is fine to have a total AUD allocation of your equity portfolio to be at most 50%. If you choose to have a small home bias, then hedged International would be more attractive, while a large home bias means that hedged International would be less attractive.

HGBL and VGAD

There is a wide variety of hedged equity products to construct a DIY portfolio, but I’ll be focusing on the two most popular ETFs to hedge the international market: HGBL and VGAD.

Before I go on, an extra consideration that hedged products have is whether they use ToFA. If a hedged ETF doesn’t adopt ToFA, then the ETF becomes incredibly inefficient from making excess distributions. PIA explains further what ToFA is here. VGAD used to not have ToFA in the day but finally adopted ToFA at the end of June 2024. ToFA isn’t an important consideration these days, as most hedged ETFs adopt ToFA now. Although VGAD uses ToFA now, it may still be tax inefficient, as it uses managed funds to hedge the currency (source from this reddit post).

Below are the ETF details:

| HGBL | VGAD | |

|---|---|---|

| Management Expense Ratio (MER) | 0.11% | 0.21% |

| Assets Under Management (AUM) | $2.56 billion | $6.85 billion |

| Index | Solactive GBS Developed Markets ex Australia Large & Mid Cap Index AUD Hedged | MSCI World ex-Australia, hedged into AUD Index |

| Replication strategy | Representative sampling | Full replication |

| Inception date | 16/05/2023 | 18/11/2014 |

For another article on currency hedging, I would recommend: Illuminvest – Currency Hedging Explained for Australian Investors.